What if I were to tell you that there’s a simple yet almost guaranteed way of becoming a millionaire, even if you start today earning below average salary and have literally 0 assets? In this article, we will go through the simple yet highly effective method to becoming a millionaire, even if you had a low starting point in the current tough market conditions.

By the global standard, a millionaire is someone with net worth of over US$1M dollars. According to Wikipedia, only around 9% of US adult populations are millionaires, and most other countries except Switzerland and Australia have even less millionaire percentage. Based on a 2021 global wealth report published by Credit Suisse, there are only 1.1% of populations have reached the 7-figure mark. It’s safe to say that becoming a millionaire is definitely not easy.

Is it even possible for a regular Joe with below average income and $0 assets to become a millionaire? Assuming there are no lottery tickets, no outsized windfall.

To answer this question, let’s do some quick calculations based on a couple of assumed scenarios.

Savings and Retirement Account Only

Meet Joe, a 24 years old fresh grad with zero assets, earning a yearly salary of $43,789 US dollars, equivalent to the average US fresh grad salary in 2022. He contributes 4.5% of salary to 401(k) with matching co-contribution from his employer, on-par with the average (For those who are not from the US, 401(k) is a type of retirement account, similar to Superannuation in Australia, Workplace Pension in the UK, MPF in HK, and so on. Most countries have something similar). He puts away 10% of remaining salary to a regular savings account receiving an average of 0.06% interest, and spends the rest. Probably not the best financial arrangement considering inflation and the low savings rate, but let’s see how far this takes him through time.

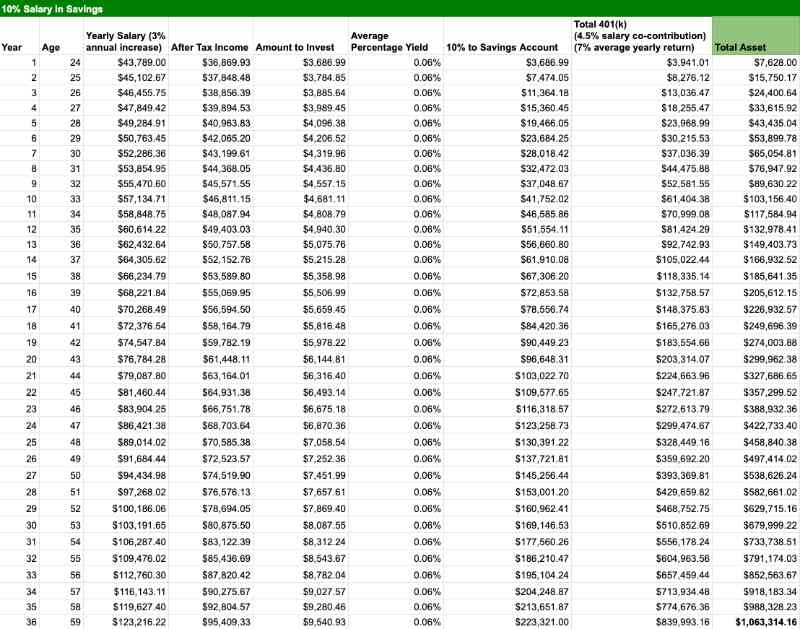

By the end of year one, Joe has $3,941.01 in his 401(k), and $3,686.99 in his savings account, therefore his total asset is $7,628 (Note: for simplicity, first year interests and 401(k) growth is discarded.)

At the beginning of the 2nd year, Joe gets a standard pay rise of 3%. Assuming his 401(k) gets a decent 7% yearly returns, which is around the average of similar retirement saving plans, and if he continues with the same 10% savings rate with the same interest rate of 0.06%, by the end of year 2, he would have $15,750.17 in total asset.

Now, let’s assume that Joe has a very stable career and holds the same job with an average 3% yearly pay rise throughout his entire career. With the same 10% savings rate receiving the same 0.06% interest rate, and the same 4.5% retirement account co-contribution at 7% average yearly return rate, his total asset, which consists of the cash balance of his savings account and retirement account, would reach a total balance of $1,063,314.16 by year 36.

In other words, Joe becomes a millionaire at age 59, ahead of the average retirement age of 62. This is quite astounding, considering only less than 9% of US adult populations are millionaires, yet Joe, starting at age 24 with below average income and ZERO asset, can become one of the top 9% of US population, by simply holding a steady job, moderate yet consistent savings habit and retirement account contribution.

Index Fund Investment and Retirement Account

The greatest investor Warren Buffett is a huge fan of the S&P500 index fund. What if instead of depositing 10% of salary into a savings account that pays almost nothing, Joe invested the same amount regularly into the S&P500 index fund? When will Joe be able to reach the millionaire status?

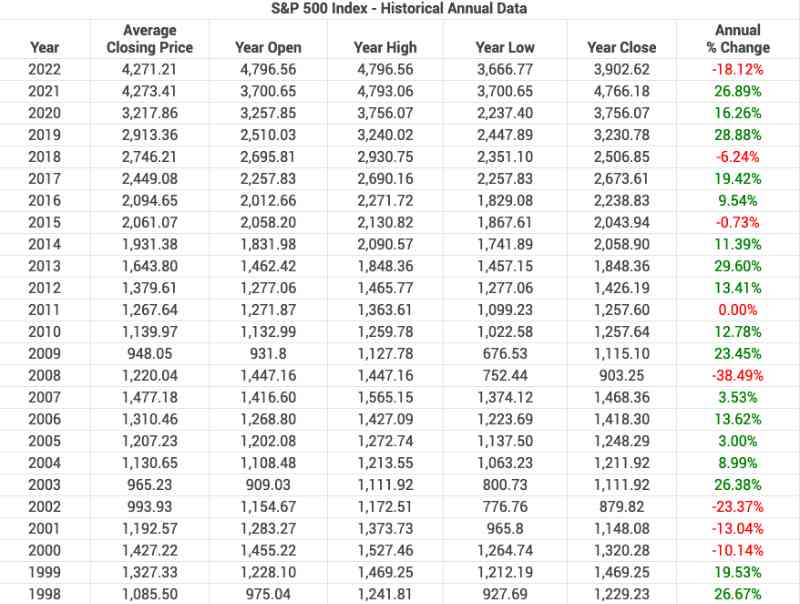

To make this simulation more realistic, let’s take the actual S&P500 annual return rate into consideration, starting from 1999, right before the DOT-COM bubble stock market crash from 2000 to 2002 (see below).

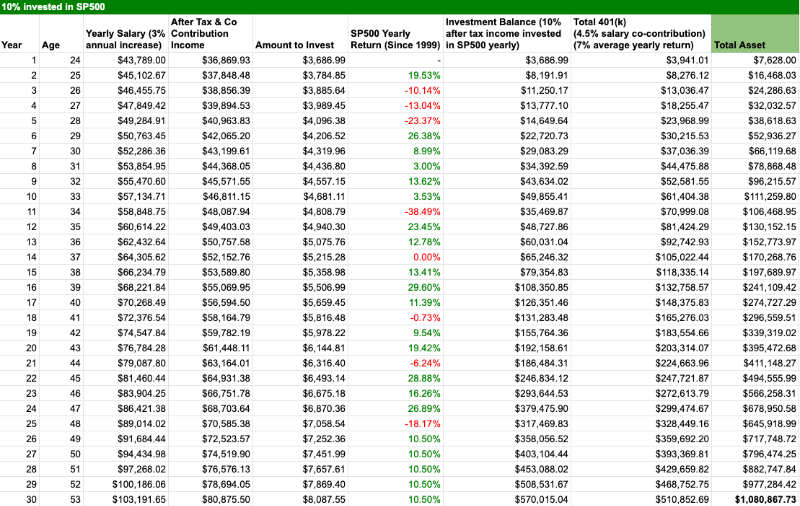

Assuming everything else remain the same, and the only adjustment is Joe’s investment approach with his 10% salary. By the same calculation method, combining his S&P500 index fund investment and retirement account balance, Joe would be able to amass $1,080,867.73 of total asset in 30 years, by age 53!

What if instead of only investing 10% of his salary, Joe decided to be more disciplined and invested 20% of salary in the S&P500? He would become a millionaire in 24 years, by age 47!

Earning Minimum Wage?

What if instead of earning an average salary, Joe started with the US minimum annual salary of $15,080, but still invested 10% of his after tax income consistently in S&P500 and kept the same retirement account contribution? He would become a millionaire by the age of 63, on par with US average retirement age.

Remember, these calculations have taken all of the stock market crashes since 1999 into consideration, including the dot-com bubble crash and the 2008 great recession.

Conclusion

I know this calculation is based on some ideal world assumptions such as non-interrupted income with consistent pay rise, but I also discounted the potential of more significant pay rise opportunities such as promotion or job changes.

The moral of the story is that you don’t need to be exceptional to become a millionaire. With consistent income, regular savings, index fund investing, and continuous contribution to retirement accounts, even with a slow-start, your chance of becoming a millionaire is much greater than you think.

Due to high inflation, rising interest rate and the fear of a potential recession, the S&P500 index is on track to have the worst first half of year since 1970! Is this the worst time to get in the stock market as the market may continue to go down? Or, is it a generational buying opportunity based on billionaire investor Ron Baron and Wedbush Securities managing director Dan Ives? Only time will tell.

One thing is certain, despite the economic condition, simply by protecting your income stream, consistently put as much money as you are able into low cost investments like an index fund and retirement account, the chance of you becoming a millionaire is not IF, but WHEN.